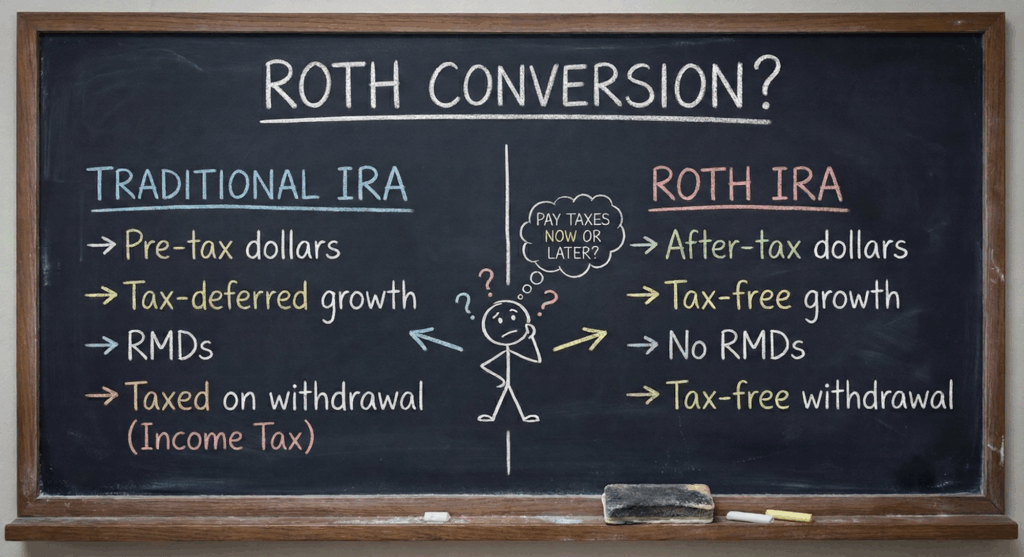

It’s that time of year again when investors with Traditional IRAs consider converting some (or all) of those IRA assets to a Roth IRA.

One of the most common questions we get asked involves the strategy of converting a Traditional IRA to a Roth IRA. While financial headlines often paint this as a universally smart move, the reality is that the decision is rarely black and white. Knowing folks with vastly different income levels and balance sheets, I can tell you that this is one of the most personal financial moves you can make. It relies almost entirely on the specific nuances of your life, meaning what works perfectly for your neighbor might actually be a mathematical mistake for you.

The core of this decision comes down to a comparison of tax rates and your willingness to make a bet on the future. You have to ask yourself if you would rather pay the tax bill on that money today at your current known tax rate or gamble on what your tax rate might look like in retirement. This involves analyzing your current income and trying to forecast what the tax environment will look like ten or twenty years down the road. You are essentially volunteering to take a hit to your wallet now to secure tax-free growth for the future, but that only makes sense if the math works in your favor.

You should also think beyond your own timeline and consider the people who might eventually inherit these assets. A major part of the strategy involves deciding whether you want to absorb the tax cost yourself so your spouse, children or or other beneficiaries do not have to deal with it later. By converting now, you might be saving your beneficiaries from a massive tax headache during their own peak earning years. It comes down to whether you want to leave them a tax-free gift or a portfolio that still has a hefty mortgage to Uncle Sam attached to it.

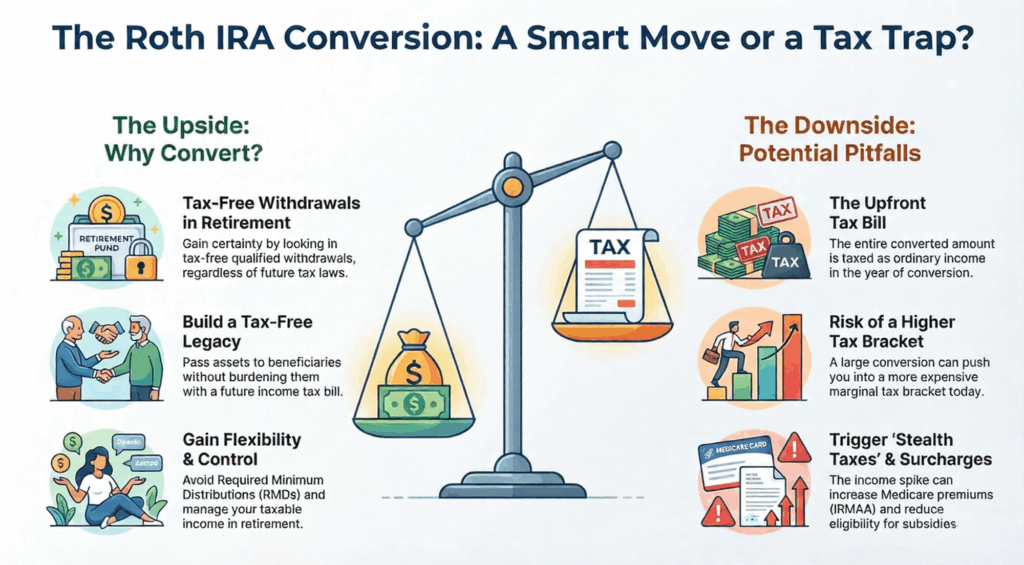

Here is a breakdown of the potential pros and cons to help you weigh your options.